Tracking your clients’ numbers and sending monthly reports isn’t enough. Yes, the numbers are an important tool for their business. But without any financial literacy, that data remains unopened.

As business owners, your clients want to make a profit. Unfortunately, a percentage of your clients possess financial shame. How the numbers work remains a mystery to them.

Some symptoms of financial shame include the following:

- Fear and anxiety about their cash flow.

- Fail to grasp the meaning behind basic reports.

- Decisions influenced by emotions rather than data.

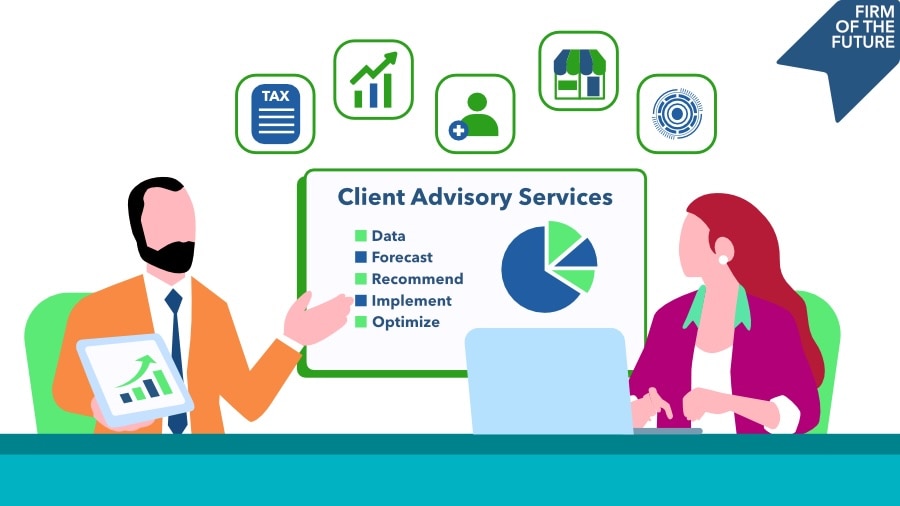

That’s why a growing number of accounting and bookkeeping professionals regularly meet with their clients. These consultative meetings are a dedicated time to translate the reports. Then, discuss how the data applies to their business.