The 2026 Small Business Late Payments Report maps five pressure points in the payment cycle. Here's where advisors can make a difference.

70% OFF QuickBooks Advisory Bundle for new clients

News

Late payments, processing delays, and manual processes: new data on the cash-flow gaps your clients are navigating

Key findings:

- 59% of small businesses have invoices overdue by 30+ days, up from 47% last year. Businesses waiting on unpaid invoices are owed $17.7K on average.

- Businesses that require immediate payment are less likely to end up with overdue invoices. 64% of businesses with no overdue invoices require upfront payment, compared with just 34% of those with overdue invoices.

- Nearly 2 in 5 owners (39%) say one late payment made it hard to cover payroll or bills in the past year.

- 49% of owners say standard payment processing times create critical or moderate cash-flow gaps, even after the customer has already paid.

- 59% paid a fee for instant transfer or fast deposit in the past year. For 15%, it's a recurring expense.

- 74% of businesses aren't fully automated on bill pay. Manual work is the top internal reason for delayed outgoing payments across the board.

You've seen it in the books already. A client with solid revenue but a persistent cash-flow problem. Invoices sitting open past 30 days. A credit card balance that keeps climbing. An owner who hasn't paid themselves in weeks.

The 2026 Small Business Late Payments Report puts numbers to what a lot of advisors are already seeing across their client base. Drawing on data from the Intuit QuickBooks Small Business Insights survey and the 2026 Business Ownership report, it follows the money through the full payment cycle: from invoice sent to payment received to funds actually available to use. What it finds is friction at every stage, with small business owners absorbing the brunt of the cost.

Here's what the data shows, and where the advisory conversation starts.

The five pressure points

For most small businesses, the payment cycle has more than one weak spot. And the pressure points don't operate in isolation: money gets stuck in one place, and the strain moves to the next. Most clients are dealing with more than one of these at a time, which is why a cash-flow problem that looks straightforward on the surface often isn't.

1. The invoice.

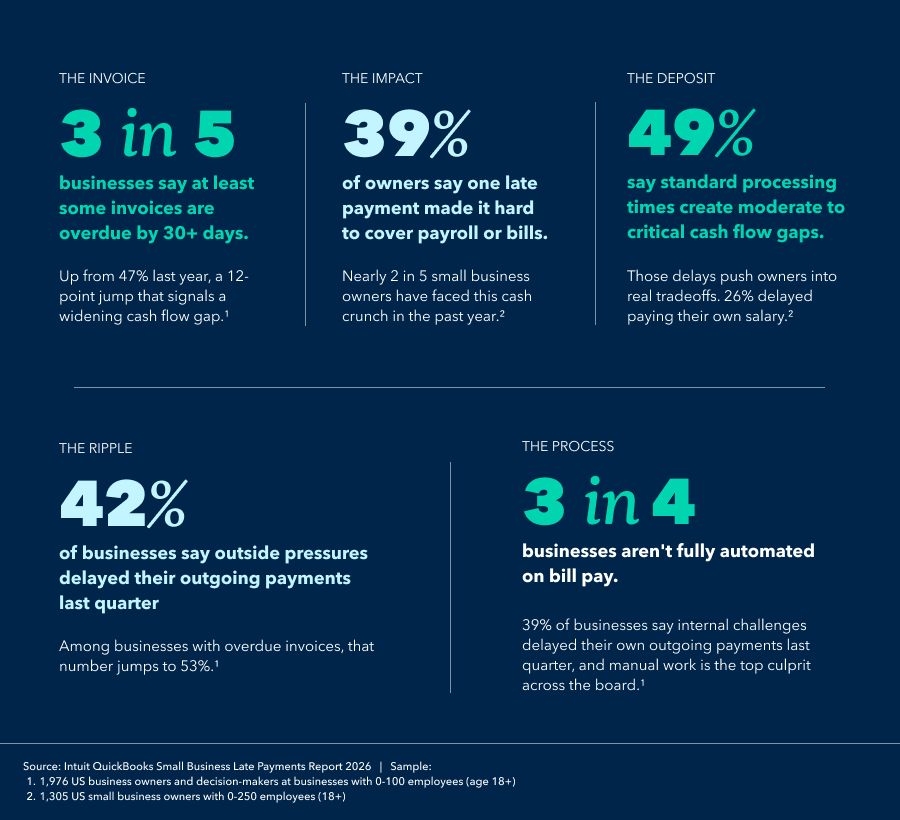

Nearly 3 in 5 small businesses (59%) have invoices overdue by 30 days or more, up from 47% last year. The average business waiting on unpaid invoices is owed $17.7K. For 1 in 5 businesses, more than 20% of their invoices are past due.

2. The impact.

The downstream effects hit faster than many owners expect. Nearly 2 in 5 (39%) say one late payment made it harder to cover payroll or bills in 2025. The breaking point is small: 27% say a missed payment under $5,000 made it harder to cover payroll or bills, including 12% who say a late payment under $1,000 was enough to cause a strain.

3. The deposit.

Even after a customer pays, the money isn't always ready to use. Nearly half (49%) of owners say standard processing times create critical or moderate cash-flow gaps. Those delays push owners into real tradeoffs: 26% delayed paying their own salary, 19% took on debt they otherwise wouldn't have, and 18% paid a bill late and incurred a penalty.

4. The ripple.

When a business is waiting on money, its own vendors and contractors wait too. 42% of businesses say outside pressures delayed their outgoing payments last quarter. Among businesses with overdue invoices, that number jumps to 53%.

5. The process.

Internal friction compounds the problem. 39% of businesses say internal challenges delayed their own outgoing payments last quarter, and manual work is the top culprit across the board. 74% of businesses aren't fully automated on bill pay.

Where advisors fit in

The data points toward five places where the advisory conversation can make a real difference. The full payment cycle has a lot of moving parts, and small businesses don't always see how they connect: how payment terms affect overdue invoices, how processing delays push owners toward credit, how late incoming payments ripple out to delayed outgoing ones. Advisors who can see the whole picture, and help clients understand where the friction is building, are in a position to do something most clients can't easily do on their own.

Payment terms are a cash-flow lever.

Requiring payment upfront makes a measurable difference. Among businesses with no overdue invoices, 64% require immediate payment. Among those with overdue invoices, only 34% do. The more time a business gives customers to pay, the more likely those invoices are to go unsettled: more than half (55%) of businesses on net-30 terms have overdue invoices, compared with 26% of those on immediate terms.

That's a structural risk that shows up in the books before it ever becomes a collections problem. Pulling up a client's standard payment terms and walking through the tradeoffs isn't just an invoicing conversation. It's a cash-flow conversation.

Cash reserves matter.

When a single missed payment under $1,000 can threaten payroll, that's not just a collections problem. It's a reserves problem. When the threshold is that low, the issue isn't just that customers are paying late. It's that there isn't enough of a buffer to absorb normal timing gaps. For advisors, that's a meaningful distinction.

Helping a client chase overdue invoices faster addresses the trigger. Helping them build a cash reserve that can absorb a slow week or a missed payment addresses the root cause. The data makes clear how thin the margin is for a lot of businesses, and that's exactly the kind of thing clients often can't see clearly on their own.

The cost of instant transfer adds up.

59% of small business owners paid a fee for instant transfer or fast deposit in the past year, and for 15%, it's a regular occurrence. That's a line item that often doesn't show up anywhere until someone looks for it. Advisors can help clients see what they're actually spending to access their own money, and whether there are tools that reduce or eliminate that cost.

The pressure owners feel around payment speed and fees is also showing up in Washington. In April 2026, lawmakers introduced the PACE Act, a bill aimed at giving qualified nonbank payment providers direct access to Federal Reserve payment systems, which could mean faster transfers and fewer fees down the line. It's not a fix advisors can offer today, but it's worth knowing about when a client asks why instant transfer fees exist in the first place.

Cash flow forecasting stops the ripple before it starts.

Most owners know when their own payments are running late. What's harder to see is the pattern. Among businesses with overdue invoices, 53% say outside pressures delayed their own outgoing payments, compared with just 26% of businesses without overdue invoices. And 24% of businesses with overdue invoices say delayed revenue was the direct reason they couldn't pay their own contractors, suppliers, or vendors on time.

When advisors help clients map incoming and outgoing payments together, late payments stop being surprises that trigger a scramble. Clients who can see a shortfall coming have options: follow up on overdue invoices earlier, communicate proactively with vendors, or make deliberate decisions about which payments to prioritize. Clients who can't see it coming are just reacting.

Automation isn’t optional.

Manual work doesn't just slow things down. It creates risk. 74% of businesses aren't fully automated on bill pay, which means nearly 3 in 4 clients are managing some version of this friction manually, often without realizing how much it's costing them in time and errors.

Owners already see where automation could help. The areas where they see the most potential for AI: reminders to pay bills (40%), data entry (37%), spending insights (33%), fraud detection (32%), matching bills to the right expenses or payees (32%), cash-flow recommendations (29%), and making payments (28%). These aren't aspirational use cases. They're the exact tasks that eat up time, introduce errors, and slow down a payment process that doesn't have much room for either. Advisors who can help clients identify where manual work is creating the most friction, and match them with tools that remove it, are addressing both sides of the cycle at once.

The bigger picture

The late payment problem isn't new. But the data makes clear it's getting worse, and it doesn't stay contained to one part of the business. It moves through the payment cycle, from overdue invoice to cash-flow gap to credit card balance to delayed vendor payment, picking up cost at every stage.

The advisors who help clients build fewer places for money to get stuck aren't just doing better accounting. They're doing better advising. And that's a different kind of value.

For the full data breakdown, read the 2026 Small Business Late Payments Report.

Recommended for you

Get the latest to your inbox

Get the latest product updates and certification news to help you grow your practice.

Looking for something else?

Call Sales: 1-844-435-1308